Civitas Continues to Deliver Peer-leading Free Cash

| Price $48.05 | Dividend Holding | December 15, 2024 |

- 4.2% base dividend, 50% of free cash flow going toward share repurchases.

- Colorado regulatory uncertainties have historically pressured valuations, but the early 2024 agreement has delayed major risks until 2028.

- Civitas has partially shifted to the Permian Basin, emphasizing cost reduction in drilling operations rather than outright production gains.

- Still some minor expansion in DJ Basin, advancing with 4-mile lateral drills in premium-priced high-grade oil.

Investment Thesis

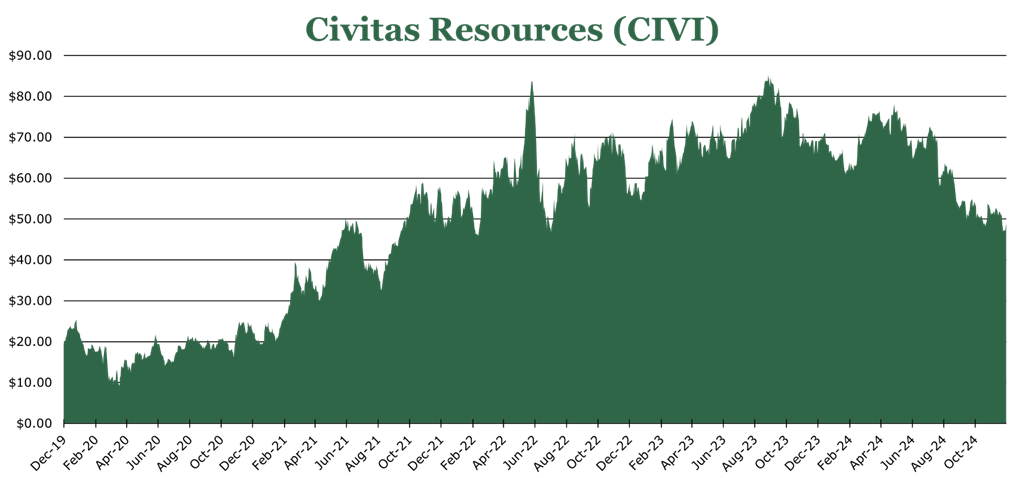

Civitas Resources (CIVI) is an oil and gas company operating in the DJ Basin in Colorado and has recently expanded into the Permian basin in Texas. Despite decreasing costs per boe (barrel of oil equivalent) and regulatory uncertainties being resolved until 2028, the stock has been hammered harder than other energy peers, losing 29.42% on a YTD basis.

Even in the face of slumping energy prices, Civitas has strong free cash generation ability which should support the base dividend of $0.50 per quarter, currently yielding 4.20%. Additionally, management is shifting the variable dividend to a mix of share repurchases and improving the health of the balance sheet. Given that strong base dividend will be maintained, we believe that Civitas is a solid income stock with potential price tailwinds from repurchases and risk repricing.

Estimated Fair Value

EFV (Estimated Fair Value) = EFY25 EPS (Earnings Per Share) times P/E (Price/EPS)

EFV = E25 EPS X P/E = $9.75 X 9.0 = $87.75

A P/E of 9.0x would bring CIVI in line with Permian-weighted Peers and better reflect the dividend and high share repurchase levels.

| E2024 | E2025 | E2026 | |

| Price-to-Sales | 0.9 | 0.9 | 0.9 |

| Price-to-Earnings | 5.5 | 4.9 | 4.4 |

Overview

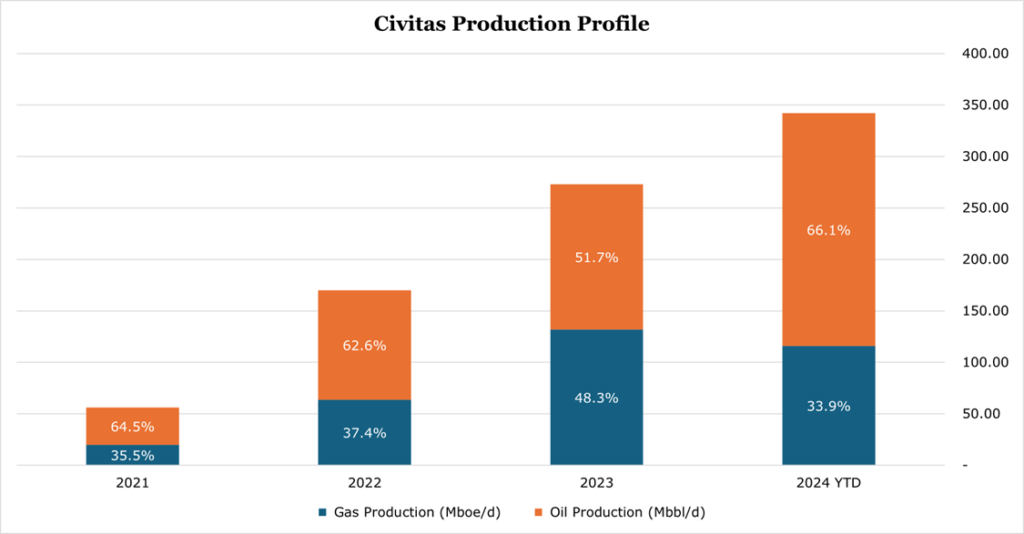

For a larger overview of operations, see our last report. On a YTD basis, the production profile is 2/3 oil and 1/3 natural gas, though Civitas can shift production to more gas if there are pricing tailwinds as it did in 2023.

| First 9 Months of 2024 ending September 2024 | DJ Basin | Permian Basin |

| Crude Oil Production (Mbbl/d) | 101.7 | 124.4 |

| Crude Oil Realized Price ($/bbl) | $75.91 | $78.11 |

| Natural Gas Production (MMcf/d) | 466.4 | 397.8 |

| Natural Gas Realized Price ($/Mcf) | $1.80 | $-0.71 |

| Natural Gas Liquids Production (Mbbl/d) | 53.8 | 69.4 |

| Natural Gas Liquids Realized Price ($/bbl) | $24.30 | $18.36 |

| % Of Total Production | 47.4% | 52.6% |

For the first 9 months of the year ending September 2024, total sales volumes were up 81% to 342 Mboe/d (thousands of barrels of oil equivalent per day). Though, the low hydrocarbon pricing environment meant that revenues were up only 67% over the same period.

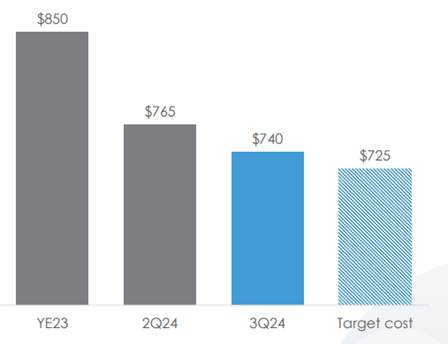

Since the start of 2024, Civitas has added more than 75 wells in the Permian which will continue to make up most production increases. Civitas is trying to bring down the drilling costs to the $725/drilled lateral foot range to make its operations there competitive on a per boe basis with the DJ basin. For reference, the DJ Basin has historically had a $700/ft cost. For the quarter ending September 2024, oil represented 47% of Permian output, with most of the natural gas produced is sold at a loss due to oversupply conditions.

Civitas now considers the DJ Basin a “legacy asset” but noted that it is still undergoing limited drills in the Watkins area. The Watkins area has higher quality oil than the rest of the DJ Basin and thus usually trades at a slight premium to WTI (West Texas Intermediate). Drilling activity in the area is utilizing new techniques, including Civitas’ first 4-mile laterals. Given the harsher Colorado regulatory environment, 4-mile laterals is an indicator that Civitas is trying to maximize production with as few wellheads as possible to avoid regulatory cost. For the quarter ending September 2024, oil represented 44% of production in the DJ Basin.

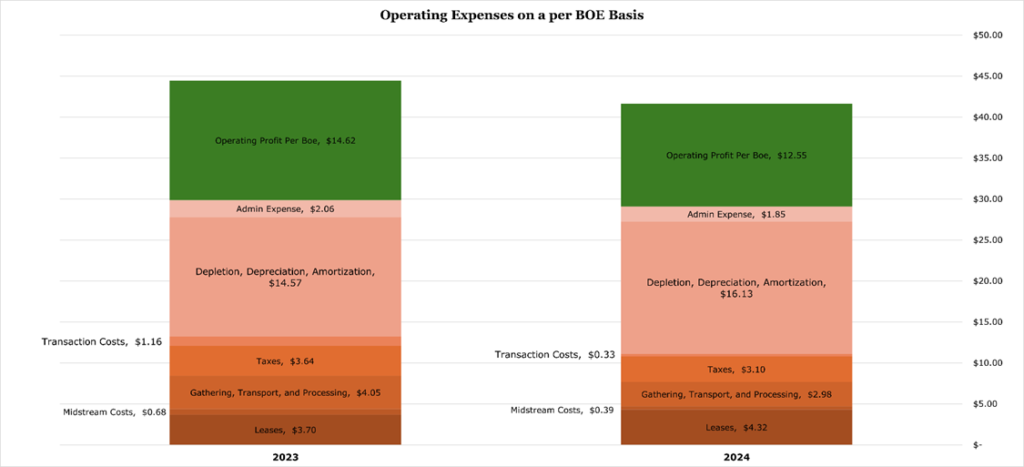

On a per BOE basis, operating expenses increased to 72% of realized price from 65%. This is due to the expanded footprint and low hydrocarbon pricing. Permian leases typically have a premium over the DJ Basin, and the higher pace of Permian drilling has driven up depletion accounting charges. All other metrics decreased on a per BOE basis, and we expect there to be good cost leverage once oil or gas prices begin to move upward.

The Discount

Civitas trades at a discount relative to peers and has seen -29.42% YTD return despite an improving cost profile and its footprint expansion. There are some secular factors we discussed in our article on TotalEnergies, such as global oil demand continuing to be low, which has driven poor price performance across the energy sector. However, Civitas’ discount has historically been driven by regulatory concern in Colorado, which in our view is over-priced into the stock.

Colorado’s oil and gas sector faces regulatory pressures which have historically had companies heavily weighted in the region trade at a discount compared to peers more heavily weighted in states like Texas (namely Occidental and Chevron).

The regulatory environment started to become stricter with SB-181 in 2019, which shifted the COGCC’s (Colorado Oil and Gas Conservation Commission) mission to prioritize environmental protection over resource development.

The ongoing regulatory battle between the Colorado government, activist groups, and oil companies exploded in early 2024. At the time, there were 3 bills in the state Congress, and several potential ballot measures for the 2024 election that would ban fracking or impose harsh penalties on operators. In April, Governor Polis brokered a deal between major operators, environmental groups, and representatives of the state Congress to drop anti-fracking ballot measures and block additional legislative action until 2028.

To reconcile all parties SB-230 and SB-229 were introduced, which impose production fees based on current prices and formally codifies additional emission targets. The fees are to be calculated quarterly based on a rolling spot price average, and levied as $0.12/bbl for every $10 oil moves over $40/bbl. For natural gas, it is levied as $0.0048/Mcf per every $0.40/MMBtu increase of natural gas prices.

| Oil Price ($/bbl) | Fee ($/bbl) |

| <$40 | $0.04 |

| $40-$50 | $0.12 |

| $50-$60 | $0.24 |

| >$60 | +$0.12 per $10 |

| $76.37 | $0.44/bbl |

The fees will begin to be levied in July 2025. If the fees were presently levied in the current quarter, they would be around $0.44/bbl for oil and $0.0112/MMBtu for natural gas. These fees would lower free cash by approximately $6 million, or less than 2%.

For 2025, Civitas estimates that it will average an oil fee of $0.45/bbl, and $0.25/Mcf, which implies a flat oil price, and increased natural gas prices, with production flat.

| Natural Gas Price ($/MMBtu) | Fee ($/Mcf) |

| <$1.40 | $0.0016 |

| $1.40-$1.80 | $0.0064 |

| $1.80-$2.20 | $0.011 |

| >$2.20 | +$0.0048 per $0.40 increase |

| $2.11 | $0.0112 |

Post-2028 is much more difficult to predict. In the earnings call for the quarter ending September 2024, management stated that Civitas is focusing on flexibility of production with the driving force behind non-maintenance capex being on driving costs down to maximize free cash with the current footprint. Much of the risk could be mitigated by the time any ballot measure or legislative action would have significant impact on operations.

Civitas has a long-standing positive relationship with the Colorado government and has operated as carbon-neutral in the state since 2021 (through purchasing offsets) so it may be spared significant cost on regulation focused on emission targets.

Risk

The largest risk to Civitas operations, aside from regulatory, is that their natural gas is traded at a discount due to transport constraints. Civitas operates minimal midstream infrastructure of its own, with the majority of both basins in-field gathering, compression, and transportation being third party. Winter tends to see favorable natural gas pricing in the DJ Basin as 70% of Colorado households use natural gas as heating, which can create a local premium to NYMEX prices. However, the oversupply in the Permian of natural gas has led prices into the negative for several quarters.

Civitas typically hedges around 30-40% of its output, which is about average for peer producers. However, with oil prices potentially staying below $80/bbl for longer, the hedging ratio for oil may increase to lock in better realizations – especially if the Trump admin pushes for more US output.

Financials

During the quarter ending September 2024 earnings call, management stated that growing production is a lower priority than driving costs as low as possible. Macroeconomic concerns globally and regulatory concerns in Colorado have made Civitas more apprehensive about building out production at a faster scale. By the end of 2025 Civitas will have a better picture of how it wants to position itself over the longer-term. As a result, we expect Civitas to keep production flat in 2025 though it may see some cost leverage increasing margins as the year goes on.

Capex for 2025 is expected to be much more level than the front-loaded nature of 2024 given the flat production target. If oil prices continue to decline into the $60s range, it is likely that Civitas will let oil production contract in the Permian, which could lower capex for the second half of 2025. On the other hand, if oil moves back up to the $80 range, Civitas may want to jump-start additional production in the Permian and potentially increase capex in the second half of the year.

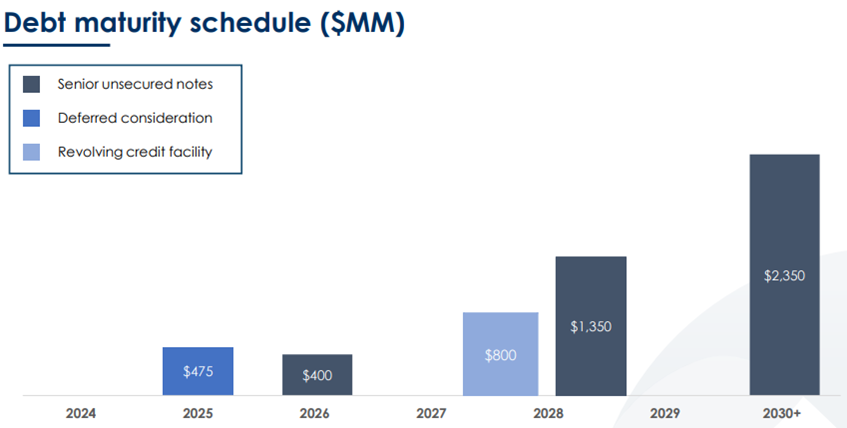

Debt levels are elevated compared to the historical average, due to the number of acquisitions. As of the quarter ending September 2024, Civitas had a net debt to EBITDA of 1.3x, compared to the pre-Permian average of 0.25x. It is unlikely that management will take more M&A action with the stock price trading so low and current leverage levels.

Despite the large increase in debt, in August 2024 Civitas was upgraded to BB+ by Fitch, with the agency stating that the increase in production in a more regulatory friendly environment should support strong liquidity and free cash flow.

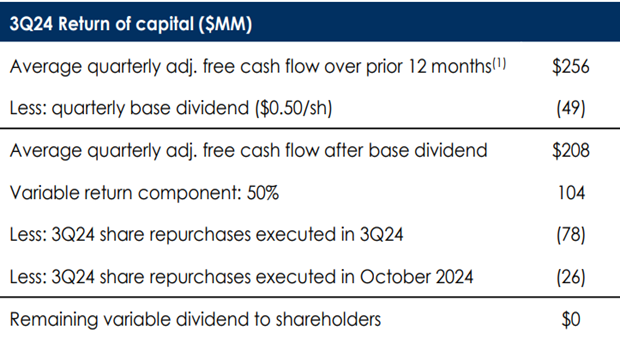

or the trailing 12 months ending September 2024, Civitas generated $962 million in free cash flow. The shareholder return profile is shifting more toward share repurchases rather than the variable dividend. The new free cash priorities post-dividend are 50% to reduce leverage, and 50% to repurchase shares.

If the post-dividend free cash stays in the $200 million neighborhood, Civitas could repurchase around 2.1% of its outstanding shares per quarter. This is on top of its $0.50/share base dividend, yielding 4.2%.

Conclusion

Overall, the risk posed to Civitas operations has been mitigated until at least 2028. Despite management cutting the variable dividend, the base 4.2% yield is still highly attractive when paired with the quarterly share repurchases. Thus, despite the slump in hydrocarbon pricing, Civitas remains undervalued relative to peers.

Peer Comparisons